My last post on Developer Experiences introduced APIs (Application Programming Interfaces) & use cases they enable. Often referred to as the plumbing beneath the modern application development infrastructure, APIs are everywhere. Visa’s controversial $5.3B Plaid acquisition effort and the PSD2 mandate enforced in Europe were just the latest high profile examples that spotlighted this. In this post we dive deeper into an exciting revolution in the Fintech industry and understand the value driven by APIs.

APIs are the connective tissue that glue modern applications today. These can be an organization sharing valuable information, enabling new product experiences via different avenues, partner companies sharing information with each other to drive more end user value, or organizations simply exposing their platform as a ecosystem that external developers can build on – APIs are everywhere. They are the building blocks of a world where monolithic applications (think a giant hard to move rock) are broken down into micro services (think tiny pebbles that are much easier to manage and talk to each other to make up that bigger rock) to enable faster, more innovative application development. Still unconvinced? – here are 3 ways you likely have interacted with an API today:

Checked the weather on your iPhone this morning?

An underlying API connects your weather app to data from companies such as weather.com or accuweather. It dynamically polls for this information to keep you updated. Fun fact: weather companies see 100000x more traffic via these exposed APIs compared to their website.

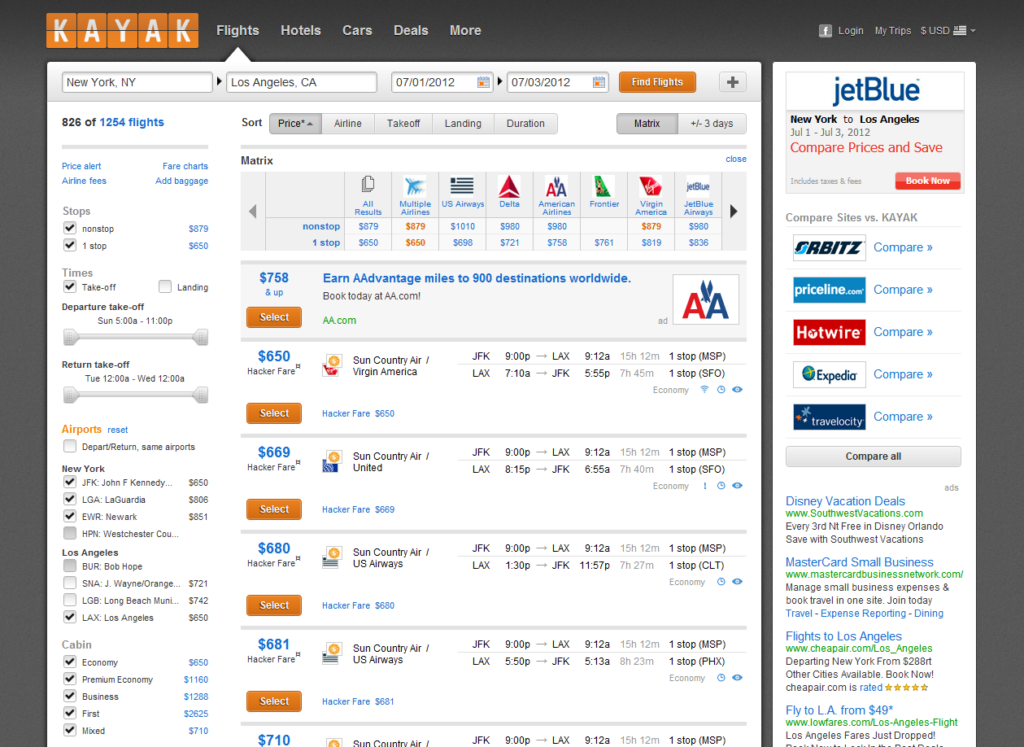

Planning a cheap getaway and did a flight search on Kayak?

Kayak uses APIs to pull information from various airline providers such as Delta, United, American Airlines, etc, aggregates this data and shows you the summary so you don’t have to click through 1000s of websites and apps

Shopping for holiday gifts on Amazon?

Amazon is the pioneer of the modern microservice driven app experience. Amazon.com brings together 1000s of their internal teams (recommendations team, shopping cart term, furniture catalog team, etc) to provide an overall marketplace like experience.

The financial industry is traditionally conservative. An unwillingness to share proprietary data, solitary risk averse initiatives, and a general lack of innovation has been typical of the industry. This mostly is for all the right reasons – managing finances is a big responsibility and the smallest misstep can have huge implications on individuals or entire economies. The benefits to fostering innovation have always been outweighed by the risks involved, until recently! The rise of APIs has changed this very cost-benefit tradeoff – APIs are increasingly used to drive secure relationships between entities, fundamentally changing traditional assumptions. These relationships are between different organizations or within the same organization and aim to foster much faster innovation. Let’s look at two examples of how this works:

The PSD2 Mandate

The revised Payment Services Directive (PSD2) regulation went into effect in Europe last year. The mandate has two key components – Strong Customer Authentication (SCA) and Open Banking. Diving deeper, there are many layers but at a high level, both components are focused on requiring financial institutions to expose proprietary data and payment services within their platform via APIs in a safe, standardized manner to enable innovation.

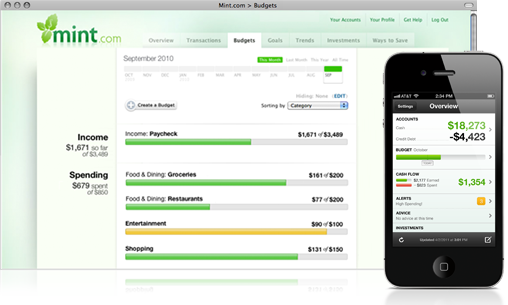

Consider mint.com – an aggregator of finances for individuals. Mint.com uses APIs to build secure relationships with different financial institutions and retrieve user data as long as the individual provides consent. A user with finances spread across many financial entities can now have a single aggregated view of their financial health on the app. This reduces complexity that comes with managing one’s finances and empowers users to make smarter decisions. Another example is Trustly – an app that empowers consumers to directly use their bank accounts to pay for expenses. By providing an alternative to credit card networks, Trustly avoids unnecessary approval loops, chargeback fees, and enables a single payment system for businesses dealing with different currencies. Trustly too has built relationships with banks across the world facilitating a more seamless experience for the end consumer.

In a nutshell, by mandating PSD2 regulations European regulators hope to open the financial sector to more collaboration and innovation driven by the Mint.com and Trustly’s of the world. They hope to offer consumers more choice, and ultimately a richer smarter experience.

The Plaid Story

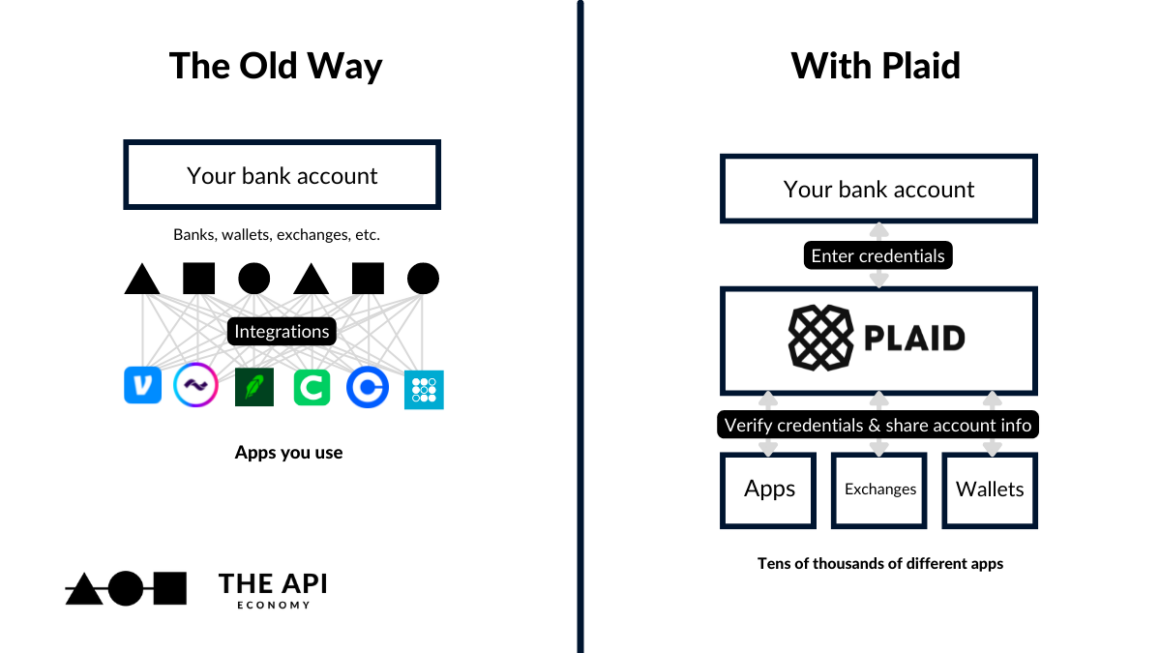

Plaid, founded in 2013, goes a step further to the companies we mentioned above. It aims to be the connective tissue under in a world where collaboration among financial institutions is table stakes. Unlike mint.com or Trustly, Plaid does not focus on specific use cases – it simply acts as a technology layer that enables applications to connect with user bank data by building relationships on both ends.

Plaid focuses on two critical value propositions that enable this layer:

- An ecosystem of hundreds of partner financial institutions and applications that it has built relationships with. Their financial ecosystem partnerships here include 9,600 partners today including all the prominent household names.

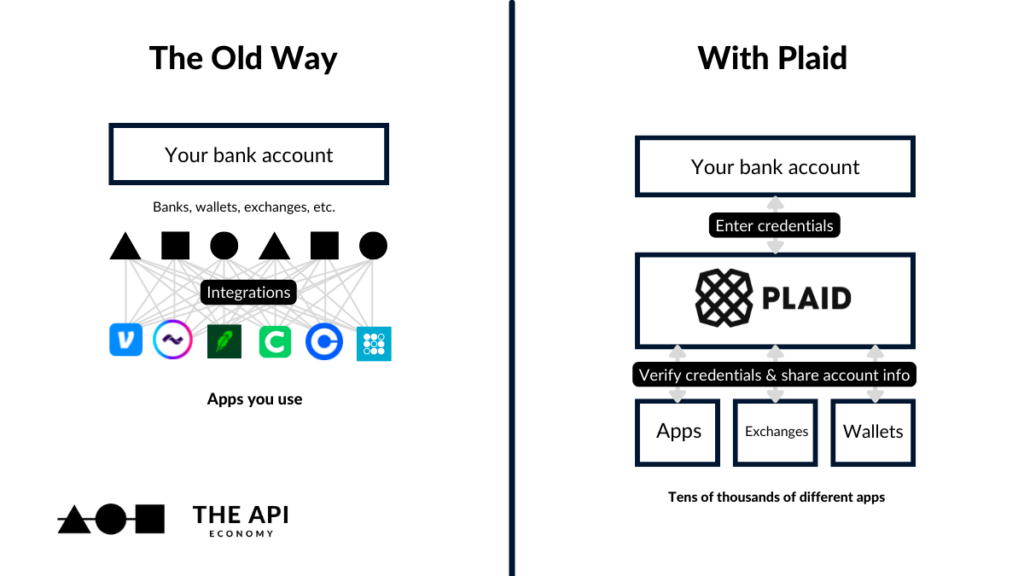

- Providing a single extremely reliable API that abstracts away the complexities that come with dealing with APIs for different institutions. APIs have a learning curve and it can often be difficult to get familiar with individual APIs for different organizations. Furthermore different applications and organizations might have different security standards, and the ability to trust a partner is key in developing an API based partnership. Plaid abstracts this out by building a simple, standard, secure interface on top with individual organization and application APIs. For example, notice their API endpoints here – a simple set of extremely secure public facing APIs are connecting to individual APIs belonging to different institutions under the covers. Individuals or businesses wanting to build their own integrations don’t need to know about these – they simply leverage and trust the Plaid layer.

It should be apparent by now why Visa is paying a premium to acquire Plaid. Trust based credit card transactions powered by Visa form the foundation of payment networks around the world. That world is changing – and Plaid’s business model and technology stack directly play into the Visa’s very value proposition. By acquiring the company, Visa hedges its bets today and is prepared for the new world tomorrow. The examples above are only two among many recent and expected upcoming moves within the financial sector, fueled by an API-first economy. The key term we have reiterated in the example above is trust based partnerships. Secure APIs today are the engine below this, and drive innovation in a more collaborative, connected world.